“Smart Homes” – An Analysis of Emerging Business Models and Pricing Strategies

Over the last few years, communication service providers (AT&T, Verizon) as well as cable operators (Time Warner, Cox) have been pioneering the concept of a “smart home” as a one-stop solution that satisfies their customers’ needs for safety, security, convenience, et cetera. Although the conventional idea of a “smart home” has struggled to gain relevance, technology advances in the areas of broadband connectivity, networking and managed services are enabling an ecosystem that becomes the foundation for increased consumer adoption. Consequently, service providers have been tenaciously trying to up-sell their smart home services.

This makes a lot of business sense, especially for those consumers who need these services at an affordable price point, but the operational realities are quite complex. This article discusses some of them. Beginning with a brief description of a smart home and the different elements of its value proposition, it analyzes the industry’s value chain and the different business models that can be conceived. It then discusses their pricing strategies and provides recommendations on how industries can identify new metrics and models to create sustainable competitive advantages.

So, What Is a “Smart Home”?

A smart home is one in which multiple devices can be remotely monitored and controlled based on the needs and preferences of its users/residents. For example, residents can monitor security, watch kids play or observe elders for their safety, record programs on DVR, turn off electrical appliances, adjust their thermostat, or turn on their cars. The different components of a smart home include services related to security, utilities, entertainment and healthcare.

The different elements of a smart home value proposition can be aligned with its related services:

Services | Key Value Proposition to End Users |

Monitoring |

|

Energy Management |

|

Entertainment |

|

Health care |

|

What Is the Smart Home Market Opportunity

Currently, the smart home market is generating annual revenues of US $25 billion1. It is estimated that by 2017, the market size for the smart home industry in the US will be US $60 billion2. The corresponding European market is expected to be worth $3.2 billion by 20153.

All of this data points to significant potential for industry growth but there are is a concomitant set of challenges that can be divided into two broad categories:

- Consumer awareness

- Industry/business models

Many consumers are not fully aware of the benefits or the value from their homes becoming smart. Further, they are worried about losing privacy, essentially with the overhead that comes from managing multiple, inter-connected devices. Finally, some customers have specific needs for which they may not be willing to pay a premium. So, it is imperative that service providers develop viable business models and value propositions for the mass markets.

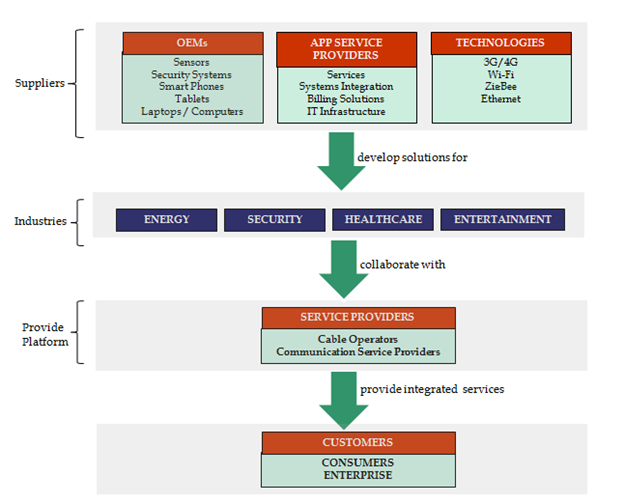

Figure 1 illustrates the industry’s value chain that acts as the foundation for conceiving multiple business models. They can range from one in which a service provider acts simply as a “connectivity provider” to one that “owns” every element of the service component. Neither one is operationally feasible. A viable business model is based on “partnerships” between several industries such as utilities, health care, security, and entertainment with service providers to offer integrated solutions and a consolidated bill to customers.

This partnership-based model leads to significant advantages in economies of scale and scope with key capabilities in the areas of service enablement, shared distribution/sales channels, and scalable backend systems for billing, CRM, et cetera. Significant synergies can also be derived from key activities such as network support, customer service, marketing, analytics, and product/service management.

Besides, each partner must continually adopt new technologies and identify business models that maximize value for customers and profits for the group. This is possible by focusing on and agreeing to optimizing costs and identifying new revenue streams. Some of them are listed below:

Optimizing the firm’s cost structure by addressing

- Increase in fixed costs (due to network rollout)

- Increase in operating expenses (due to network maintenance and infrastructure support)

- Reduce customer acquisition costs

- Reduce customer service costs

- Increase in platform development costs

Identifying new revenue streams

- Platform management fee

- Value-added service fee from partners

While the partnership model has several benefits, significant issues can come up over disagreements in sharing revenues, go-to-market strategies, operations, customer service etc. Typically, negotiations over revenue-sharing arrangements tilt in favor of those companies with a reputed brand and a large, loyal customer base. In this case, service providers, with their larger customer base, have the lead but sustainability is not guaranteed.

Figure 1: Industry Value Chain

Figure 2 lists the major service providers in the US, along with their respective smart home brands and pricing packages. Most of them use a subscription-based pricing model, with monthly recurring charges and a one-time charge for equipment installation. Since the primary target market is existing subscribers, who are already used to this model, this strategy makes a lot of sense. However, as markets mature and services become more commoditized, partners should renew focus on:

- Effective customer segmentation – Redefine segments to profitably increase market share, primarily attracting non-consumers.

- Analytics – What features are essential to each segment of customers and what is their relative willingness to pay?

- Metrics – Focus on those metrics (Avg. revenue per user, customer lifetime value, customer acquisition, Retention and Service Costs etc.) that yield fresh perspective on the state of the business.

Armed with some new insights, service providers should employ some of these tactics in a creative and aggressive manner:

- Promotions and Discounts – These can be used extensively to lure non-consumers.

- Bundling – B2B partnerships must be created and offers bundled; this would increase penetration and market expansion.

- Life-cycle pricing for individual products and bundles should be analyzed carefully to conduct targeted campaigns and increase renewals.

Figure 2: Service Providers and their respective “Smart Home” Brand Offerings

Service Provider | Brand Offering | Features | Pricing Packages |

| Comcast | Xfinity Home |

| |

| Cox Communications | Home Security Services |

| |

| Time Warner Cable | Intelligent Home |

| |

| AT&T | Digital Life |

| |

| Verizon | Home monitoring and control |

|

- Juniper Research

- Vision for Smart Home, GSMA

- http://www.machinetomachinemagazine.com/2011/05/01/european-smart-homes-market-worth-3267-million-by-2015/

- “The Connected Home: Evolution of the Consumer Space” by Frost and Sullivan

- “Broadband Forum Value Proposition for Connected Home” by Broadband Forum; Issue Date: April 2011

- Gartner’s report “Cool Vendors in Consumer Energy Management, 2012”; Published on: 20 April 2012 by analyst(s): Jim Tully, Van L. Baker, John Girard, Alfonso Velosa, Derek Prior, James F. Hines, Simon Mingay

About The Author