Bombardier CSeries: How will Boeing/Airbus Duopoly Respond?

The much-anticipated Bombardier CSeries commercial airplane line provides a uniquely positioned offering, boasting 20% fewer CO2 emissions, 20% fuel savings, and 15% less cash operating expenses than comparable alternatives. With expected fulfillment of initial CSeries orders occurring in mid-to-late 2013, Bombardier poses a significant threat to the once dominated duopoly market of passenger fleet 100 to 149 seat capacity aircrafts. Over the next decade, Bombardier’s CSeries product line specifically targets Airbus’ A320 and Boeing’s 737 aircrafts with the intentions of capturing at least 50% of current market share enjoyed by the heavy hitters.

Airline manufacturing analysts predict a demand of approximately 34,000 new commercial aircraft over the next 20 years. The most fruitful subset (68%) of the entire commercial fleet market rests in the 100 to 149 seat capacity segment. With Bombardier inching at the heels of the big two and commercial airlines demanding more efficient airplanes, how will the market landscape adjust and distribute the market share up for grabs?

The Bombardier CS100 and CS300 are roughly priced at list around $65 and $75 million, respectively, which falls almost 18% below the list price of the Airbus A320 and 5% below the list price of the Boeing 737-800. The value proposition delivered by the CSeries aircraft in comparison to market competitors is demonstrated in figure 1.

Figure 1: Bombardier’s Value Proposition

Bombardier CSeries aircraft is positioned as value advantaged in the commercial airplane manufacturing market space. Since the CSeries offerings deliver superior value to customers relative to competitors at lower list prices, Bombardier’s go-to-market pricing strategy is consistent with a penetration pricing methodology. Bombardier’s aggressive entry tactics for the CSeries aircraft offers a credible threat to existing Boeing and Airbus revenue.

With over 382 commitments for CSeries aircraft from customers including Korean Air, Luxair, and airBaltic, Bombardier proves it is serious about delivering cost-effective airplanes to consumers seeking better margins. Rick Erickson, an independent aviation analyst, speaks of the Bombardier CSeries, “Once it’s up in the air and they start proving the plane’s cost-benefit — they’re arguing, 20% fuel savings — I think we’re going to see airlines fairly quickly start moving towards the aircraft.” The resilience of the air transportation market even in economic downturns, estimated 5% annual growth in world passenger air travel for the next 20 years, and passenger airlines seeking operating cost cuts, yields promising futures for airline manufacturers.

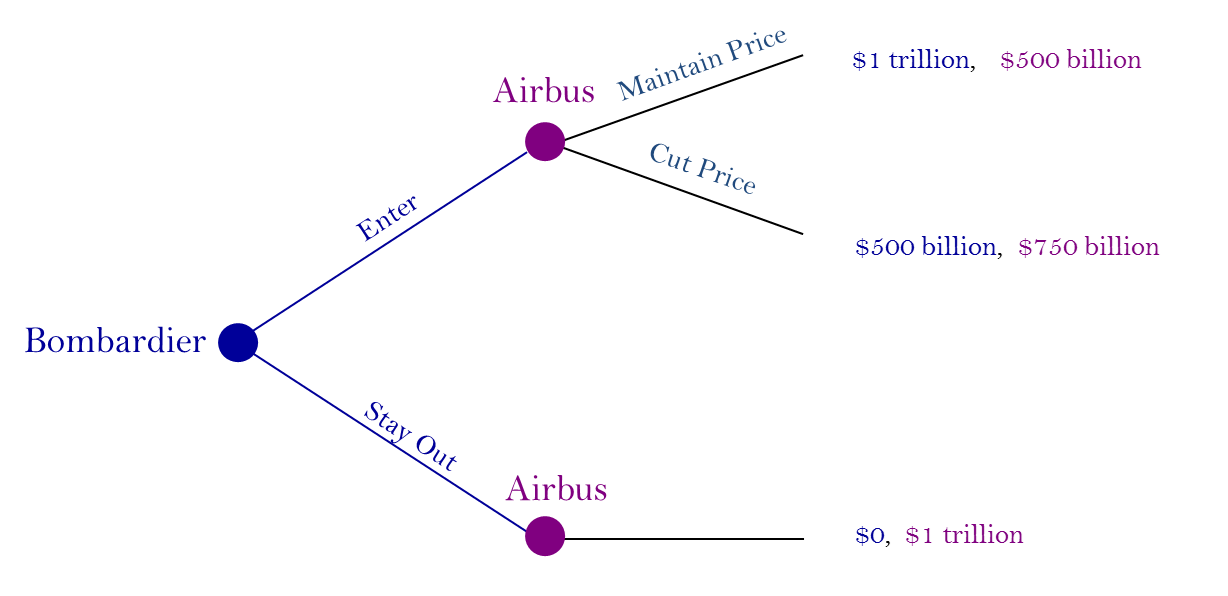

The pertinent question at hand is this: how will the dominant market powers, Boeing and Airbus, respond to a fringe firm encroaching on their market share and revenue? Will the larger relative market cap companies, Boeing and Airbus, choose “predatory” tactics to combat such advances by Bombardier? And by what means will Boeing and Airbus approach this market invasion? Several countering techniques could be employed to mitigate market share loss including price concessions to meet the competition, volume and customer loyalty discounts, or other promotional incentives. The incumbents need to decide which method will allow for acceptable market share loss with respect to reasonable margin deterioration. Figure 2 shows the decision events and outcomes associated with employing a price-to-meet-competition strategy.

Figure 2: Price to Meet Competition Decision Tree

Figure 2 explores a possible distribution of revenue over the next 20 years between one dominant player, Airbus, and the entrant, Bombardier (accounting for Boeing’s revenue). It is estimated that $2 trillion worth of value exists in the 100 – 149 seat, single-aisle passenger plane market from 2012 – 2031. The subsequent statistics are founded on plausible expectations of Bombardier’s market growth strategy. Assuming that Bombardier effectively executes its 50% market-revenue capture, the following conjectures will rest.

Presumably, if Bombardier were to stay out of the market, Airbus and Boeing would split the revenue spoils and receive approximately $1 trillion each. If Bombardier enters the market as expected and supplies abundant CSeries airplanes, Airbus has options to maintain its current price level or offer price discounts to meet competition.

If Airbus does not change its pricing strategy for the current A320 aircraft:

- The market will realize that its aircraft are value disadvantaged.

- It will potentially lose $500 billion, realizing $500 billion in revenue.

- Given Boeing making a decision similar to Airbus’, Bombardier stands to bank $1 trillion.

- Boeing would take the remainder of the available market revenue.

If Airbus grants price concessions to be more competitive or rectifies its price-to-value alignment:

- Bombadier will earn approximately $750 billion.

- Airbus and Boeing (again, assuming comparable strategy decisions) split the rest of the market, each receiving $750 billion.

Employing a price-to-meet-competition strategy, Airbus would more than likely experience some revenue bleed-out, but would avoid losing half its revenue to Bombardier. Bombardier’s market-growth rate would be partially thwarted by such discounting tactics employed by Airbus.

The outcome of this market entry scenario can be derived through backward induction. Airbus would choose to cut its price if faced with entry from Bombardier to salvage potentially drastic revenue loss. Bombardier evaluating its potential revenue gain would choose to enter the market due to $1trillion (Enter) exceeding $0 (Stay out). The outcome of the game delivered is a (Enter, Cut Price) outcome. Of course this analysis is purely speculative, but has grounds based on best-observed pricing practices. More robust studies would explore multiple decision trees encompassing both incumbents and the entrant, account for probabilistic choice, and move-order significance.

Other means of observing market interaction in the aviation manufacturing market would prove useful in providing further insights on expected incumbents’ actions. Needless to say, Airbus and Boeing’s key line of revenue and primary source of growth going forward is at stake. Without strategic pricing direction and market execution by the dominant firms, the current duopolistic market may be a thing of the past.

Dr. Saul Barr and Robert E. Mansfield, Jr., Aerospace Economic Report and Outlook for 2010, (Embry-Riddle University, 2010), 193.

Bombardier 2011 Annual ReportAirbus 2013 List Price Sheet: Aircraft A320

http://www.boeing.com/commercial/prices/index.html

http://www.boeing.com/commercial/cmo/index.html

9 Comments

About The Author

Your article refers to the 727. I think you mean the 737. Boeing stopped making the 727 twenty nine years ago.

Does the author mean the Boeing 737, not the 727?

most of the information in this article is utter garbage. The market for 100-150 seats is far less than 10% of commercial jet aircraft deliveries. The CSeries, while ultimately a good aircraft when going into service in 2014, will never exceed more than 50-100 units per year. It is also much smaller than the 727, and smaller than most of the members of the 737 and A320 families

Our apologies on the error replacing “737” with “727”. It has now been corrected.

The fact is that when both Airbus and Boeing have decided to re-engine A320 and B737 with more efficient engines they have increased dramaticaly the number of orders, and CSeries has orders are still a small fraction

Perhaps you didn’t notice. Boeing and Airbus have both re-engined versions their competing aircraft. Judging by the massive order volumes for these jets, it would seem that airlines have a different view of the Bombardier value proposition.

Airlines buy into families of aircraft.

Bombardier will struggle with sales for a few years. Till they launch the 150-165 seat CS500. That’s when the ball game will change.

The A319/B737-700 are both too small and too heavy, even with their new engines to really offer what most airlines want: close to 150 seats. Bombardier is particularly positioned to deliver at optimized aircraft at that capacity.

According to Leahy of Airbus, the airframe will only contribute to 3% of fuel efficiency and the engines the rest. If he is correct, then this means that a similar size Boeing or Airbus with the same engine as a CS will deliver savings or penalties in the 3% region. This can be wiped out if the MRO options available are not favourable to Bombardier. The duopoly has been in the game for a long time and support companies will offer MRO contracts to suit their expertise and base of spares or parts. Bombardier will have to create a subsidised MRO network to support the CS- otherwise they will at best be a niche player.

Leahy is paid to say those things. He’s the head of sales for Airbus. What else would he say? When he had the same engine on his 320s going agaist the 737s, he said the airframe was everything. For the sake of credibility, I wouldn’t quote Leahy as having said anything.