What Exactly Is Target Transaction Pricing?

For many manufacturers and distributors making the initial transition from cost-plus pricing to value-based pricing, their first hurdle is to strategically define the price on each and every transaction. How exactly should they do it? What will the process look like? How can a strategically defined value-based price reflect the realities of competitive dynamics, customer needs, and marketing aims?

Target transaction pricing is a well-trodden approach to managing all these needs.

Target transaction pricing is used in companies ranging in industries from bubble wrap to specialty chemicals, fabricated metal, and many others. It allows for dynamic flexibility, tactical clarity, and managerial oversight. It enables both strategic price management and tactical price variance allowances.

What follows is a technical note on target transaction pricing.

Target Transaction Price Is…

Conceptually, a target transaction price is the price at which the company expects a salesperson to close a specific deal.

Notice the deal specificity. Target transaction prices are deal dependent. That means it can vary between customers and between selling opportunities with the same customer. Target transaction prices may be customer dependent, product mix dependent, quantity dependent, promotional timing dependent, competitive situation dependent, or even cost dependent.

The difference between target transaction pricing and purely tactical pricing is that the target transaction price is defined through strategic decisions, not purely deal specific tactical decisions. And, these strategic decisions apply to all deals that meet the pre-defined parameters.

The target transaction price is what the company expects salespeople to be able to hit, at least some of the time. Tactical pricing alone fails to give salespeople a target to achieve. Without a reasonably defined target, there can be little expectation that salespeople will achieve reasonable prices in all their deals.

Mathematically, the target transaction price is the list price minus planned discounts. That is, for many companies:

Target Transaction Price = List Price – Standard Discounts – Strategic Discounts — Promotions

That is, the target transaction price reflects the list price and all planned price variances that can be grouped as standard discounts, strategic discounts and promotions.

List Prices

The list price is the highest price a firm can expect from any deal in the market. For many companies, this is the “aspirational price” of their offerings. For others, it may be the suggested price they expect their distributors and retailers to charge end customers. Proven methods for defining list prices include Exchange Value to Customer (EVC), Discrete Choice (Conjoint), and Econometric Modeling (Statistics). Details of these approaches can be found in standard pricing textbooks such as Pricing Strategy.

Standard Discounts

Standard discounts include standard distributor or retailer discounts. These are channel discounts. For example, a manufacturer of a consumer product may expect their retailers to mark-up a product 100%. As such, they offer a standard retailer discount of 50% from the list price, and use the list price to signal to the end-customer market the suggested retail price.

Standard Discounts are generally defined for entire channels or classes of customers. For example, a producer may have a deep standard distributor discount, a moderate standard retailer discount, and a shallower standard large end-customer discount.

The size of these standard discounts tend to be industry dependent. For some firms, standard distributor discounts are as deep as 70% off list price (medical product manufactures often offer standard distributor discounts nearly this deep). For others, the standard distributor discount may be a rather shallow 20% off list price (specialty chemical companies tend who to offer standard distributor discounts near this.)

Strategic Discounts

Strategic Discounts include planned, long-term, discounts and possibly surcharges. Unlike Standard Discounts given to entire customer channels, these tend to be more order specific. For example, a firm might offer order size, product mix bundle, customer segment, accelerated payment term, and full-truck load or other forms of shipping discounts. It may also require surcharges related to rush orders, or other special orders which increase the cost-to-serve in fulfilling that order.

Promotions

Promotional discounts, like strategic discounts, are planned sources of price variances. Unlike strategic discounts, they tend to be short term in nature.

Promotional discounts can be related to seasonal promotions, excess inventory promotions, marketing initiative promotions, or batch production promotions. They can also be used to create a temporary price adjustment in relation to a competitive price move.

Importantly, promotions, even competitive price reaction driven promotions, are strategically planned.

Timing and Dynamics

To get a sense for the timing difference: standard discounts may last anywhere from some years to decades. Strategic discounts tend to be defined for a year with annual review. Promotional discounts often last for only a quarter, and sometimes for just a day.

By using a combination of standard, strategic, and promotional discounts, the firm can manage prices and pricing policy over business cycles and through market fluctuations. It enables dynamic pricing through policy decisions, rather than through a series of ad hoc tactical pricing decisions.

Target Transaction Pricing and Tactical Discounts

Not every deal may be expected to be closed at the target transaction price. There will still be special, unplanned circumstances that may necessitate greater discounts. Tactical discounting can still occur with target transaction pricing. As a goal, the target transaction price should represent the price a firm expects to get at least some of the time, but not all of the time, and should be the highest expectation — not the median expectation.

Many firms aim to have the target transaction price be the deal price at least 20% of the time. If the target transaction price was achieved 100% of the time, it likely means the price is too low (or the firm doesn’t allow any tactical discounts). If the target transaction price is achieved less than 5% of the time, it likely means the target transaction price is unrealistic and may discourage salespeople from taking it seriously.

Target transaction pricing adjusts a firm from operating with large, purely tactical, unplanned price variances all related to specific deals; to operating with smaller, tactically made, unplanned price variances and a few, strategically defined, planned price variances. That is, it is a means to shift from having only unplanned price variance to having some planned price variances and some unplanned variances.

To minimize tactical discounts while still allowing for the necessary and profit enhancing deal specific pricing, firms that adopt target transaction pricing typically also adopt two strong transactional pricing control mechanisms. These are profit based incentives, often in the form of Deal Points, and discount decision escalation policy. Profit based incentives reduces income of salespeople when they ask for a tactical price allowance, and thus act as a strong financial incentive to salespeople to close deals at the target transaction price. Decision escalation policy restrains discounting authority. Through profit based incentives and escalation policy, a firm uses both carrots and sticks, respectively, to drive better pricing decisions down to the point of customer engagement.

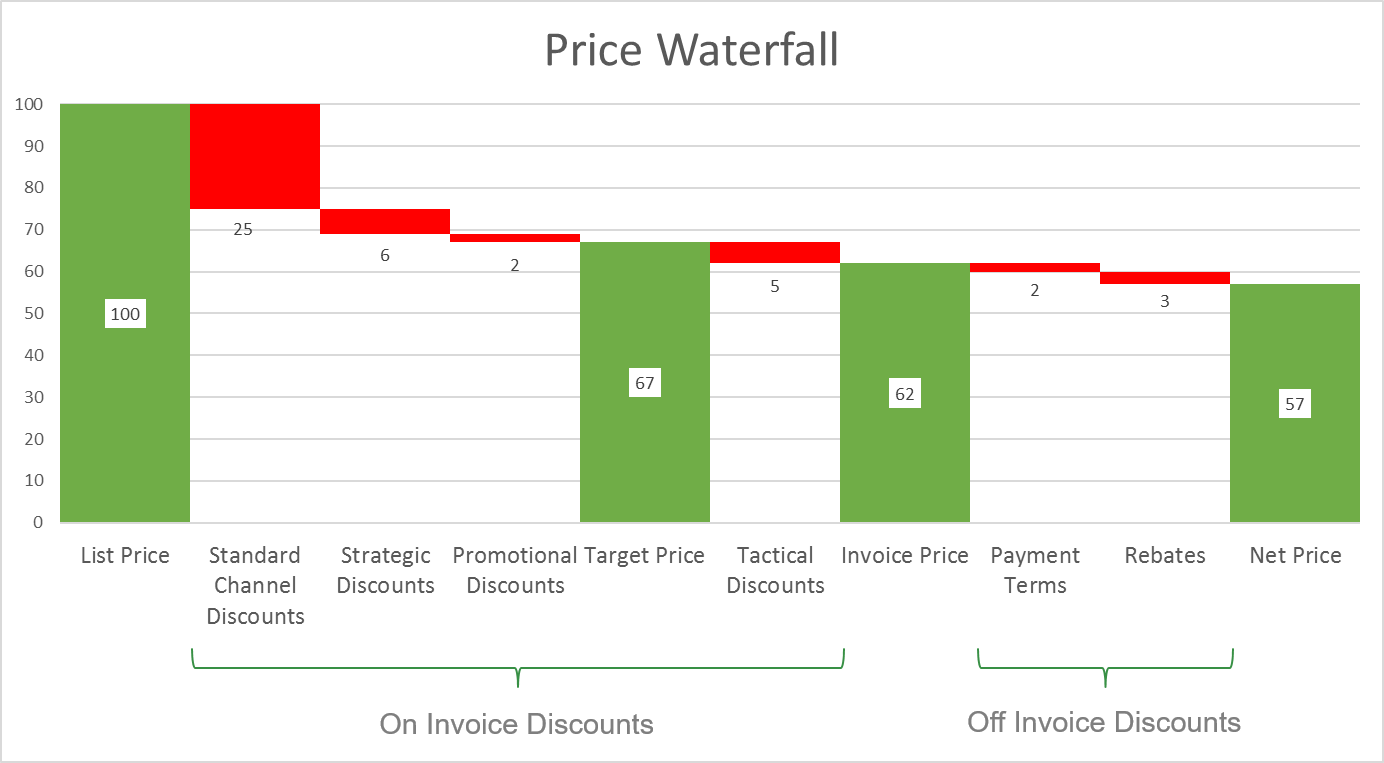

Target transaction Pricing and Price Waterfalls

Even after defining a target transaction price and managing tactical discounts, businesses may have other sources of price variances. The target transaction price less tactical discount defines the invoice price on deals. Off-invoice, the firm may allow for further discounts in the form of rebates, prompt payment discounts, or other policies. Combined, the invoice price less the off-invoice discounts define the net price of a deal.

Price waterfalls track the sources of price variances. They are a managerial tool to dissect how pricing decisions lead to the average net price. Conceptually, we can draw a price waterfall that represents all these forms of discounts, rebates, and tactical price variances as follows:

In this price waterfall, standard discounts, strategic discounts, promotions, and tactical discounts are all sources of on-invoice price variances. Payment terms and rebates are sources of off-invoice price variances. Combined with the list price, they yield the net price with intermediate price points of the transaction target price and the invoice price.

Executive Decision Making and Target Pricing

Target transaction pricing with planned discounts is often the first step in getting pricing under control. Pricing cannot be said to be “under control” when managers cannot predict what kinds of price variances they will offer, when they will be offered, or the size of those price variances. By shifting from a purely unplanned price variance policy to an at least partially planned price variance policy, executives can begin the continuous improvement cycle of making plans based on predictions, trying them in the market, measuring the results, and then improving their predictions and decisions for the next iteration. Over time, more unplanned price variances can become planned, and planned price variances can be adjusted to improve their effectiveness in enabling profitable customer engagement. See Pricing Done Right for a discussion of the continuous improvement cycle applied to pricing decisions.

Target transaction pricing with planned discounts can also reduce the frequency of executives engaging in pricing decisions. When firms rely heavily on tactical pricing decisions, executives tend to be constantly engaged in reviewing every deal with a big discount or low margin. When the move towards planned discounts in the form of standard, strategic, and promotion discounts, executive decision-making shifts its focus to reviewing pricing policy on a once a month or quarter basis. It shifts the executive decision problem from managing deal prices to managing deal policy.

Through target transaction price management, firms take a huge step towards value-based pricing. Unplanned, and therefore somewhat uncontrolled price variances are a major source of profit leaks at most companies. Unplanned price variances create a huge business risk of mispricing offers and potentially creating an unnecessary price war. By shifting towards target transaction pricing, executives can reduce the business risk associated with pricing errors, improve their ability to price offers at the point of customer engagement, and, very likely, see an improvement in profits.

It has been demonstrated year after year by study after study that a 1% improvement in price can improve profits at major corporations by 10%-13%, depending on the reporting year. This is a greater bottom line improvement than can be achieved through a similar improvement in selling more, reducing variable costs, or reducing fixed costs. Target transaction pricing with planned discount management is, for many firms, the easiest way to get that 1% improvement. Most firms, when they successfully make the transition, see a 1.5% – 6% improvement in profits.

Target transaction pricing may seem technical and detailed oriented, and making policy decisions is more difficult than making specific deal price decisions, but who doesn’t want a 1.5% – 6% profit improvement?

Interested in making the transition to target transaction pricing? Contact us at Wiglaf Pricing, Helping Executives Manage Price Better™.

Tagged: Amazon, dynamic pricing, Pricing Done Right, retail, value-based pricing

About The Author