Retroactive Rebates: Decision Inexactitudes

On more than one occasion, I have come across a curious commercial policy: retroactive rebates, and I am not alone. These retroactive rebates challenge rebate provisioning and accruals, reporting and software developers, and implementations across the globe. Yet what are retroactive rebates, why do businesses have them, and are they a good or bad thing?

Rebates are Normal

Rebates in general are negative price variances paid to customers after the invoice has been issued. They should be considered as the counterpart to discounts, a negative price variance given to customers on the invoice.

In most business-to-business industries, even business-to-business-to-consumer industries, discounts and rebates are common. They result from both planned commercial policy and customer negotiated exigencies, and are a means to shape customer behavior or accommodate competitive price pressure.

The beauty of rebates over discounts is that they can drive a customer to consider their quarterly or annual purchases with a specific supplier rather than just a single, spot purchase. For maintaining and developing long-term, mutually-beneficial, and somewhat-stable customer relationships, rebates can be a superior approach to commercial policy over discounts.

Since rebates are accrued and paid to customers later, one could state that all rebates are “retroactive” in that they impact the effective pocket price captured after the invoice is issued, and generally are issued after the invoice is paid. But that is too broad of a definition of “retroactive rebates.” Most rebates do not stir my intellectual curiosity beyond the functional need to define them and their strategic usefulness.

Retroactive Rebates are Abnormal

Retroactive rebates, the kind that I find highly curious, are most commonly appearing in distributional relationships (Pharmaceuticals, Consumer Merchandise, Energy, etc.). They are issued by suppliers to distributor to accommodate a difference between the price on the invoice at the time of the sale, and the actual competitive market price at the time the distributor resells some or all of the unit volume of that invoice.

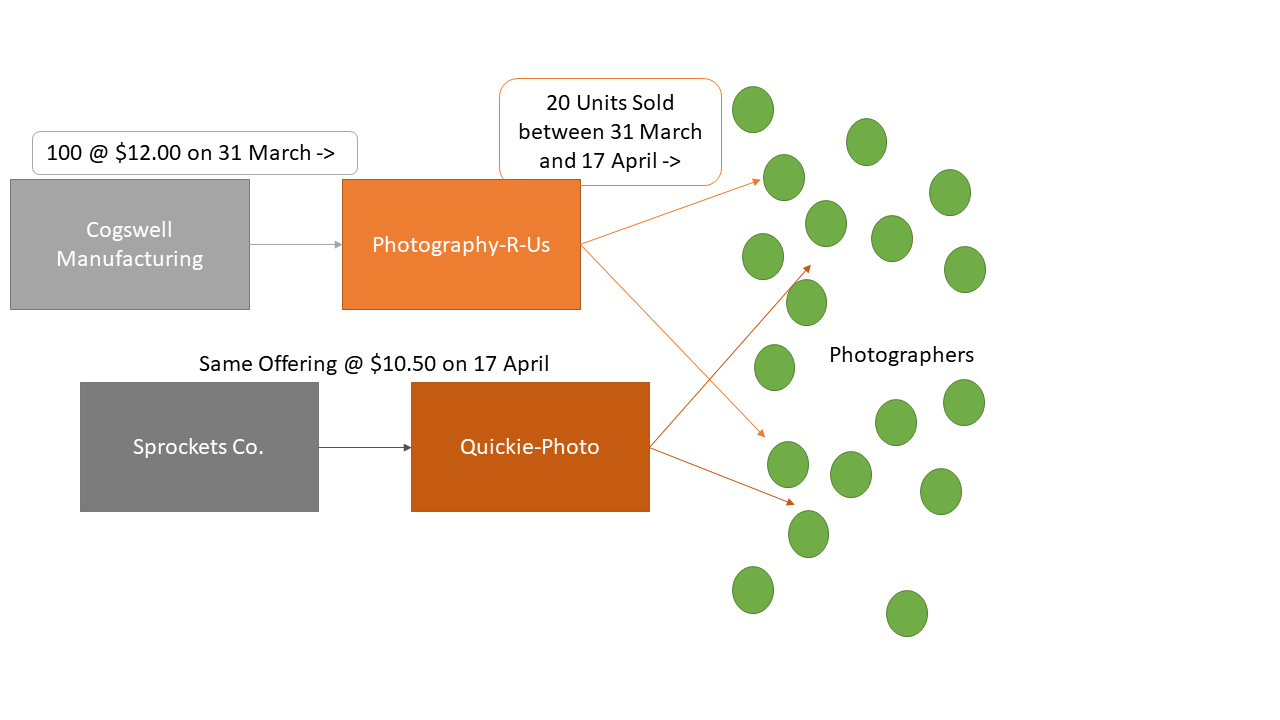

For example, suppose both Cogswell Manufacturing and Sprockets Co. make substitute camera lens filters. Furthermore, suppose Photography-R-Us and Quickie-Photo are in the business of distributing them to photographers. Similar offerings from competing suppliers sold to multiple distributors.

On March 31st Cogswell Manufacturing sells 100 camera lens filters to Photography-R-Us for $12.00 each on invoice and agrees to give a retroactive rebate if competition drives the market price down. On April 17th, Sprockets Co. sells substitute camera lens filters for $10.50 to Quickie-Photo, the direct competitor to Photography-R-Us, and offers that same price on the camera lens filters to Photography-R-Us. Photography-R-Us notifies Cogswell Manufacturing of the competitor’s offering and price, and then requests a retroactive rebate on their unsold stock. Between the 31st of March and the 17th of April, Photography-R-Us has sold only 20 units. As such, the retroactive rebate is calculated to be $120, or $1.50 on 80 units.

| Prices | ||

| 31 March Invoice Price | $12.00 | = $12.00 – $10.50 |

| 17 April Market Price | $10.50 | |

| Price Difference | $1.50 | |

| Units | ||

| 31 March Invoiced Units | 100 | = 100 – 20 |

| 17 April Sold-Through Units | 20 | |

| Remaining Units Impacted | 80 | |

| Rebate | ||

| Rebate Amount / Unit | $1.50 | = $1.50 X 80 |

| Units Eligible for Rebate | 80 | |

| Rebate Amount | $120 | |

Informational Challenges with Retroactive Rebates

The math to calculate this retroactive rebate is relatively simple. The information required to do the math however is very problematic.

How does Cogswell Manufacturing know how many units Photography-R-Us has sold between 31st of March and the 17th of April? Does Cogswell Manufacturing send a person to check inventory or do they just take Photography-R-Us’ word? Generally, the latter.

And how does Cogswell Manufacturing know the price Sprockets Co. is selling? If it asked Sprockets Co., that would be illegal price collusion in most countries, so let’s assume they don’t ask their competitors directly. Instead, Cogswell Manufacturing must learn of Sprockets Co. from its customers, and more specifically Photography-R-Us.

Is it possible that Photography-R-Us would misinform Cogswell Manufacturing of their sell-through, inventory levels, and competitor prices to get a larger rebate? Even if Photography-R-Us is an upright and honest distributor, should Cogswell Manufacturing take the word of their distributors as evidence that they should pay the difference through a retroactive rebate?

Clearly, we have an informational challenge here. Perhaps the informational requirements can be met through trust and multiple informational sources and multiple touchpoints. However, the inventory levels of distributors and the market price set by competitors will always be contentious issues in determining the size of a retroactive rebate.

Accounting Challenge with Retroactive Rebates

Even if the retroactive rebate can be calculated with clarity, one has an accounting challenge.

GAAP (Generally Accepted Accounting Principles) requires that revenue earned that is associated with rebates should be reduced by the anticipated rebate on that revenue. Generally, companies provision rebates at the time of invoicing.

How would Cogswell Manufacturing know the anticipated future retroactive rebate at the time of the sale? It could estimate the anticipated erosion of price in the future based upon history, and almost all rebate provisions are really just estimates, so perhaps this will suffice.

But in effect, Cogswell Manufacturing accounts state: “We made a sale of 100 units at $12.00 per unit to Photography-R-Us on March 31st, but we suspect the actual price is lower. How much lower, we don’t know but guess it will be $1.50 per unit lower and so we have provision for future rebates and reduced our revenue for the first quarter by $150 appropriately.”

Clearly, we have an accounting challenge here. It can be managed somewhat. SAP even has a protocol for retroactive rebates. But it must be uncomfortable to acknowledge that the company doesn’t really know what price to place on its offerings at the time of sale.

Sales Challenge with Retroactive Rebates

While I have seen companies address both the informational and accounting challenges of retroactive rebates, I can’t see them addressing the sales inexactitude associated.

Retroactive rebates call into question the definition to the associated sales. They are an acknowledgment that the sale wasn’t really made for a given price on a given volume at a given time.

The definitive moment of any sale is when the customer accepts the offering at a price at a given time. That definitive moment is indeterminate in sales subject to retroactive rebates. As such, they aren’t really sales, but rather just aspirations.

With retroactive rebates determined by competitive price moves, salespeople aren’t really driving customer purchase decisions. Customers are deciding to accept inventory, but they aren’t accepting the price to take that inventory. Rather they’re taking the price as an estimate that will be lowered in the future, and therefore they aren’t really making a purchase decision and a sale wasn’t really made.

While retroactive rebates are not out-right illegal for the situation I am writing about (as noted, we see them in Pharmaceutical, Merchandising, and Energy industries; the issue of Intel was a totally different story), they are dubious and represent a sales failure.

Pricing Challenge with Retroactive Rebates

The real challenge of retroactive rebates is their removal of price from the purchase decision. In fact, this is the main reason suppliers have a policy of granting retroactive rebates to their customers.

On near-commodity offerings, prices move every day. Suppliers may want to grant customers a price guarantee to match competitor’s prices. That price guarantee may show up in the form of a retroactive rebate. In this way, a supplier can meet their sales goals and customers can acquire inventory with the confidence that they are getting good prices. Price guarantees are common.

Price guarantees in consumer markets are usually constructed around offerings that have no exact competition, and hence do not have this same challenge. In this manner, the price guaranty a retailer makes to its consumers is no more than a statement that the retailer won’t lower their own prices. This is a very different situation than the retroactive rebates given in business markets in the promise to lower their prices.

In making this price guarantee on an offering that is known to fluctuate in price, management is somewhat abdicating their responsibility for a key decision, the pricing decision, to the market, and more specifically to their customers.

Unfortunately, retroactive rebates in business markets imply prices associated with sales can only go one way: down. In most markets, prices fluctuate both up and down. Overall, the long-term trend on prices has been upwards. In fact, central banks try to drive prices upwards in setting their benchmark rates for money to target given inflation rates. Upward price movement is the very definition of inflation.

Thus, a supplier granting retroactive rebates is effectively guaranteeing that their prices will decrease overtime even though inflation is driving up costs in general. Perhaps the downward price movements are corrected by periodic price increases, but the general motion across most time periods will be down.

Predictable Challenges

It is no curiosity to me that suppliers that grant retroactive rebates are the same entities that complain about competitive pressures and margin decreases. They designed their policies to enhance these challenges. But can management do better?

And, it is also no curiosity to me that suppliers granting retroactive rebates also tend to make a majority of their sales at the end of the month, quarter, or year. The general motivation of suppliers to grant retroactive rebates is to drive sales and hit sales goals. In truth, retroactive rebates are a very efficient means of landing the next period’s sales early and channel stuffing. But is channel stuffing a good idea?

And it is no curiosity to me that retroactive rebates increase buyer power. With retroactive rebates, customers are effectively managing the supplier’s prices, not the supplier. Customers will want to negotiate their next purchase decision based on the size of the retroactive rebate granted on the prior purchases. If the retroactive rebate is not given, or if it is not as large as they desired, the customer may choose not to purchase the targeted sales volume.

As such, the salesperson is negotiating both the size of last-period’s retroactive rebate and the current sale volume and price, simultaneously. It should be noted that the current sales price will itself be subject to retroactive rebates in the future. Quibbling about when a customer reduced what inventory in the past, when the supplier has no hard facts and is trying to meet current sales goals for the future, is a losing proposition. But should suppliers increase their direct customers’ buying power at the critical time of driving the period’s end sales? Should suppliers increase the importance of customers desire for low prices in pricing decisions?

And, it is no curiosity to me that suppliers granting retroactive rebates also become greatly concerned with the inventory level of their customers. The price they actually capture and the ability to sell more inventory to their customers are both greatly impacted by the issue of inventory sell-through. But now, we have to ask, if the distributor is charging the supplier for their sell-through, then what is the distributor doing for the supplier anyway?

At some point, the practice of retroactive rebates may drive a calamitous implosion of sales or prices, or both. But hopefully we can make a correction before then.

Correcting Retroactive Rebates

Retroactive rebates are granted precisely because prices fluctuate. While management can’t make competitors prices constant, they can make their prices meaningful.

To rid a company of retroactive rebates, management must first make sure that the prices on sales accurately reflects the competitive price in the market at the time of the sale. That is, it must continuously make informed competitive price adjustments. If properly priced at the time of the sale, that sale will not need to be repriced in the future with a retroactive rebate. This will make the invoice price a statement of fact, not an aspirational goal. And invoice prices really should be facts.

Second, management must make clear to customers that retroactive rebates are being eliminated. That is, if a customer purchases 100 units at $12.00 on March 31st, and the price moves to $10.50 on April 1st, the customer is still responsible for paying a $1,200 invoice.

Under this new approach, the customer is charged with managing price fluctuations by and between suppliers. Customer are likely to choose to purchase in smaller quantities and on a more frequent basis to reduce their risk exposure to supply price changes. But having many sales over many days between month-ends and quarter-ends is usually considered by management to be a good thing in reducing business volatility and uncertainty.

Both of these changes present a challenge to managers. The first implies that management must have the people, process, and tools to proactively manage price on a continuous basis. The second implies that management must accept the risk of having lower unit volume sales for a quarter, or possibly even a year, in exchange for greater pricing and revenue control.

And both of these changes present management with a benefit. The first implies that prices can both go up and down, and that a sale once made is a sale truly made. The second implies that sales may become more evenly distributed over the quarter and year–reducing business volatility–instead of being conducted in a frenzy at the end-of-quarter or end-of-year alone.

Are the benefits worth the challenges to drive management to make the change? Consider the alternative: further inventory stuffing, further price erosion, further margin reduction, further provisioning with uncertainty. This alternative presents a high risk for the company. Is it worth that risk simply because management finds proactive competitive price adjustments more difficult than reactive retroactive rebates? That is, they have difficulties pricing offerings right, and driving actual customer purchase decisions in the first place? Decision inexactitudes betray the lack of decisions.

Tagged: accounting, B2B, commercial policy, competitive price adjustment, distribution, Microsoft

About The Author